-California Charter Schools Association (CCSA)

Both El Camino Real Charter High School (ECRCHS) and Granada Hills Charter High School (GHCHS) were originally LAUSD public schools. While charters are marketed as a way to offer alternatives to poorly performing schools, both of these schools had excellent reputations before their conversions. El Camino has won seven Academic Decathlon National Championships, both as a charter and a public school. GHCHS “had one of the best academic records in the district [prior to its conversion], but it was bothered by cuts in district funding and hampered by rules that limited its own fund-raising abilities.” Like LAUSD schools, the teachers at both schools continue to be represented by UTLA. It should be no surprise that both of them continue to meet their academic benchmarks.

While the CCSA would like the sole focus for the judgment of both of these charters to be their continued academic achievement, the LAUSD has a responsibility to view the entire operation, including finances. ECRCHS’ "financial shenanigans” have been well documented and provide insight into a regulatory system that moves slowly and with very little public accountability. While the Notice to Cure that would eventually lead towards revocation proceedings was issued on October 28, 2015, the school’s own Governing Board was not informed until December 9. It is unclear if further action would have ever been taken by the LAUSD Charter School Division (CSD) if the Daily News had not run their own investigative report in May 2016.

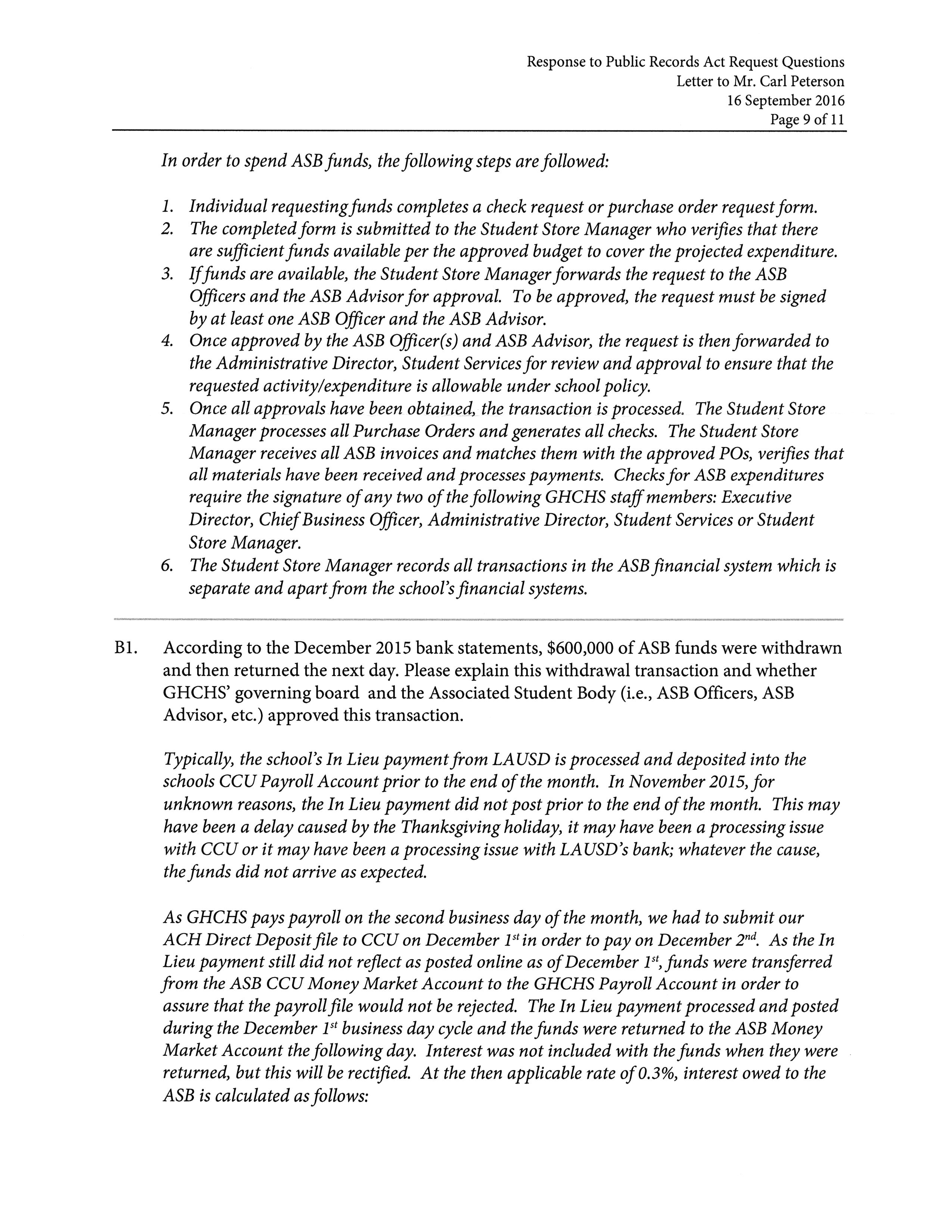

On April 14, 2016, I first reported my concerns to the CSD concerns about transfers that GHCHS had made from an account belonging to its student body to the school’s general fund. In a letter dated September 16, 2016, the charter’s Chief Business Officer, admitted that these loans took place before getting approval from the Associated Student Body (ASB) or the Governing Board. ASB funds were raised by the student body and are strictly regulated so that they can only be used for the benefit of students. They cannot be used for expenditures that are supposed to be paid through a school’s general fund. The loan of ASB funds to the general fund violated the fiduciary responsibility of the administration for these funds and generally accepted accounting principals. On September 26, I sent the following e-mail to the CSD:

On September 16, 2016, I finally received the response promised by Granada Hills Charter High School (GHCHS) during the week of August 15, a copy of which is attached. Unfortunately, with the exception of the payment of some of the interest that was due, it appears that the charter’s management has not recognized how their actions have not followed the California Education Code or Generally Accepted Accounting Principles.

Most concerning is the fact that despite being asked to “provide a list of emergency transfers from, and repayment to, the ASB account”, the “emergency transfer – LACOE ACH” of $310,000.00 on January 4, 2012, was not included in the “Emergency Funds Transfer History”. Additionally, while the loan from December 1, 2015, was mentioned elsewhere in their response, it was not included in this schedule. If GHCHS is unable or unwilling to disclose all of the transactions that I have found by reviewing their bank statements, it is doubtful that this is a full accounting of these transfers. The CSD needs to have an accountant perform a full review of the records.

The lack of care in formulating their response is apparent in the calculation of the interest due to the ASB. First, the loan dated January 4, 2012, is not included in this calculation. Additionally, even though the $25,000 on August 7, 2012, is disclosed on the “Emergency Funds Transfer History”, it is also not included in the ASB Loan Interest Calculation.

While GHCHS maintains that “ASB funds are under the control of the ASB”, the use of retroactive approvals provides evidence that this is not the case. The six step process that is supposed to be followed to spend ASB funds was clearly ignored for the expedience of the charter’s administration’s needs. If the funds were truly under the control of the ASB, then they would be frozen when the ASB was not available. Additionally, the minutes from March 26, 2012, Governing Board meeting state that “we may have to access a short-term cash flow loan from one of our investments in order to meet the July 3rd payroll”, which undermines their claim that there was not time to ask for ASB approval or that “the forecasted cash flow schedule for the school indicated that there would be sufficient cash on hand at the end of June 2012 to meet the June payroll on July 2, 2012”. It also took more than two months for this money to be paid back. This was more than enough time “to secure a bank loan or other cash flow financing to meet the school’s needs.”

Since GHCHS was not following FCMAT schedule for retention of Student Body records in 2012 and did not provide any recent minutes to satisfy my PRA requests, there is no way of determining if the ASB was provided all relevant facts when making their retroactive approvals. Were they told that loaning money to the school’s operating fund is not an approved use of ASB funds under the California Ed Code? Did they inquire about the payment of interest? Did they demand a repayment schedule? Since the money had already been transferred, were they told that they had to vote for approval? What would have happened if they voted not to approve the loan?

The fact that the administration admits that “the [2012] transfer was not taken to the Governing Board for approval” is very concerning. When the response states that the 2015 “transaction was not taken to the GHCHS Governing Board as there were not funds going from the school to ASB”, the administration is clearly ignoring the fact that the ASB funds are never supposed to be under the control of the Governing Board. Therefore, this loan was being received from a source outside the school and repayment was a contractual obligation. Therefore, the Governing Board should have approved the terms of this loan and guaranteed repayment. Furthermore, when the funds were returned, they did go from the school to the ASB.

While this response acknowledges that the transfer on December 1, 2015, was, in fact, a loan, the bank statement indicates that the transaction was classified as “Adjust GHC funds per Eugene St”. When the auditor flagged the 2012 loan, did he inform the school that these types of loans were impermissible? Was the misclassification in 2015 a deliberate attempt to conceal the nature of the transfer?

Left unanswered in the responses is why the size of the ASB has more than doubled since GHCHS became a charter in 2003. Are they prohibiting the ASB from spending this money so that they have the funds available as an emergency reserve? The administration also did not explain why the funds have not been broken up and placed into separate banks so that the full balance is covered by deposit insurance as required by the California Education Code.

Finally, the discussion about the use of ASB funds to fund athletic transportation brings up new questions about the use of ASB funds. The courts have ruled that school districts cannot charge students for participation in education activities, including the cost of transporting athletes to their games. Therefore, ASB funds cannot be used to fund expenses that should be paid for out of the general fund. It, therefore, seems highly suspect that ASB funds would be used to fund transportation.

I hope that the CSD will fully perform its function as a regulatory agency and ensure that these questions are fully answered and that the appropriate actions are taken to ensure compliance with the California Education Code and Generally Accepted Accounting Principles.

Sincerely,

Carl Petersen

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Almost a month later, I have not received any response from the CSD and there has not been any public notification that action has been taken to ensure that GHCHS has taken the steps to ensure that they will comply with the California Education Code. Unfortunately, this seems to indicate that the LAUSD’s decision earlier this month to not renew five charter schools was not an indication that the District will finally take the necessary steps needed to provide oversight or detect fraud and mismanagement of the charter industry within its boundaries.